In accordance with Article 422 of the Colombian Commercial Code, commercial companies have the legal obligation to hold an ordinary meeting of their general assembly of shareholders or board of partners at least once a year. This meeting must take place within the first three (3) months of the calendar year, establishing March 31 as the maximum deadline for its execution.

The primary purpose of the ordinary meeting is to examine the comprehensive situation of the company, determine economic guidelines, consider the state of accounts for the last fiscal year, and adopt the necessary measures to ensure the proper fulfillment of the corporate purpose.

According to current regulations, during this session, the following mandatory matters must be addressed and submitted for consideration:

Management Report: The administrators (legal representative and, if applicable, the board of directors) must present a detailed report on the evolution of the business, as well as the legal, economic, and administrative situation of the company.

Year-End Financial Statements: General-purpose financial statements, duly certified and audited, cut off as of December 31 of the immediately preceding year, must be presented, examined, and approved.

Statutory Auditor’s Opinion: For companies required to have this figure, it is imperative to read the statutory auditor’s opinion and reports regarding the financial statements.

Profit Distribution Project: The project for the distribution of generated profits must be submitted for consideration or, if applicable, proposals to offset the losses of the fiscal year.

It is essential to guarantee compliance with the right of inspection of the shareholders or partners, which allows them to examine the company’s books, vouchers, and other documents within fifteen (15) business days prior to the meeting (unless the bylaws of Simplified Joint Stock Companies – SAS provide a different term).

Failure to convene, omission in holding the meeting within the legal term, or violation of the right of inspection can result in administrative sanctions by the Superintendency of Corporations (Superintendencia de Sociedades) and affect the validity of the decisions adopted.

At BéndiksenLaw, we recommend that companies initiate the preparation of accounting, financial, and management information in a timely manner, and make the calls for meetings in strict compliance with current statutory and legal deadlines. Contact us to receive specialized counsel and ensure regulatory compliance in holding your ordinary meeting.

Since 2024 the Colombian Government tried to introduce a number of changes to the Tax Code, chiefly to increase the tax burden for taxpayers. The 2024 tax bill did not pass muster with Congress and was thus filed.

The Government then resorted to Constitutional Internal Commotion powers by means of Decree 064 of January 24, 2025, and, based on the authority granted by this decree, issued several tax reforms, whose life was limited to 2025.

Thereafter, on September 1, 2025, the president of Colombia submitted to Congress a bill for a new Financing Law, which sought to incorporate, on a permanent basis, the temporary taxes in the Internal Commotion decrees as well as other tax provisions, including:

1. Value -added tax (VAT):

Online gambling, whether operated in Colombia or from abroad, would be subject to VAT.

VAT on slot-machine gambling.

Progressive VAT basis for gasoline and other fuels.

VAT on liquor, wines and aperitifs.

Software licenses for the commercial development of digital content, as well as hosting and cloud computing services would become subject to VAT.

2. Tax increases:

Increase in the income tax rate for e-commerce from outside Colombia, from 3% to 5% of gross revenues, for nonresident taxpayers electing this mechanism.

Increase of the corporate tax rate for financial institutions from 35% to 50%

Increases of between 0% and 15%, for CIIU-0510 and CIIU-0520 coal and CIIU10610 petroleum extraction activities.

Increase in the tax rate for individuals, up to 41%.

Increase in the withholding tax rate for dividends paid from previously taxed earnings to nonresident individuals and legal entities, from 20% to 30%.

Increase to 30% for dividends paid from previously taxed earnings to permanent establishments in Colombia.

The floor for the wealth tax would be reduced to 40.000 UVT, while the maximum tax rate would increase from 1.5% to 5%.

Increase in the rate for lottery, raffles, betting and similar income, from 20% to 30% over the prize received.

The National carbon tax would increase to $42,609 pesos per CO2 ton, and adjusted yearly by the Colombian inflation plus 2%, up to $149,397 pesos per ton. This increase would also tax thermal carbon gradually, by 40% of the tax rate in 2026, 60% in 2027, 80% in 2028 up to 100% in 2029.

3. Other taxes:

The holding period for the sale of fixed assets to qualify as a capital gain and thus entitled to the flat 15% rate, would be increased from 2 to 4 years.

The 2015 1% tax on extraction and first sale or export of crude oil and coal for taxpayers with taxable income in the preceding year equal to or exceeding $2,489,950,000 Colombian pesos would become permanent under the proposed bill.

Entertainment, cultural and sporting activities would be subject to a 19% consumption tax on the ticket price exceeding $497,990 Colombian pesos.

New consumption taxes would also apply on the sale of vehicles, beer and other fermented drinks, liquors, cigarettes, tobacco and vapers.

4. Cryptocurrencies:

The transfer of cryptocurrency with underlying assets in Colombia would be taxed, as if the underlying asset itself was being transferred.

Payment of assets located in Colombia, with cryptocurrency would be considered sales of the crypto and subjected to Colombian taxation

Similarly, cryptocurrency would be deemed held in Colombia when the underlying assets are located in country. T

The providers of digital services domiciled in Colombia or with operations in Colombia would be required to report to the tax administration, all operations carried on by their users which imply the conversion of cryptocurrencies into Colombian pesos

5. Tax amnesties. On the bright side, the bill was proposing the following amnesties:

Taxpayers, omitting assets or declaring nonexistent liabilities would be allowed to regularize by paying a 15% tax on the tax basis of the assets or the tax value of the liabilities. These assets or liabilities would not be taken into consideration in determining the net worth comparison or taxable income.

Taxpayers would be allowed to pay tax, customs, or exchange control liabilities, pending on December 31, 2024, by paying the entire liability +15% of the corresponding penalty and with a reduction in interest if paid before December 20, 2025 or, if paid later and up to March 31, 2026, the penalty would increase to 40% and the interest to 50% of the banking interest rate

An amnesty was contemplated for settlement of court actions against the tax administration, where the taxpayer would agree to pay the entire tax and only between 15% and 20% of the penalty, indexation and interest.

Unpaid withholding taxes could be paid up to March 31, 2026, with only 15% of the corresponding penalties and with no interest.

Again, however, on December 9, 2025, Congress decided not to approve the bill on grounds that it was simply revenue oriented, regressive and increased tax pressure on Colombia’s middle class.

You would think this was the end of the story.

Not so.

On December 22, 2026, the President again invoked Constitutional powers, this time under Economic Emergency clause, and issued Decree 1390, that grants the President a 30-day authority to issue various decrees, including in tax matters.

No such decrees have been issued as of the date of this writing.

The reporting of exogenous information is a key process that, under various circumstances, must be fulfilled by companies and individuals, whether or not they are taxpayers of the Industry and Commerce Tax in Bogotá, withholding agents of this tax, subjects of such withholdings, and others. This tax obligation is essential to ensure transparency and the correct reporting of economic activities to the tax authorities.

What is Exogenous Information?

Exogenous information is the set of data that obligated parties must report to the District Treasury Department of Bogotá about their economic, financial, and commercial operations. These reports allow authorities to conduct effective tax control and detect potential tax evasion.

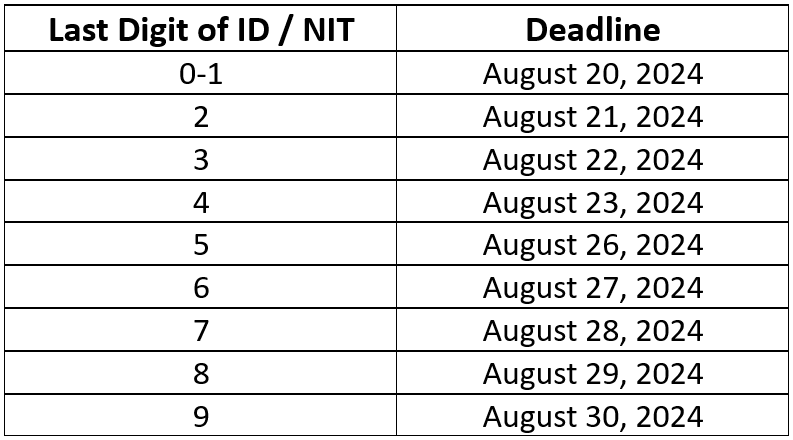

Filing Deadlines

For 2024, the deadlines for filing exogenous information in Bogotá are clearly established, and it is crucial to comply with them to avoid penalties. Responsible parties must submit the corresponding information between August 20 and 30, 2024, according to the last digit of their ID or Tax ID Number (NIT):

It is important to be mindful of these deadlines and prepare all necessary documentation in advance.

Filing Method

Exogenous information must be submitted in magnetic media, following the formats and technical specifications established by the District Treasury Deparment. Ensuring that the reports meet all technical requirements is crucial to avoid rejections and possible penalties. The filing method includes:

1. XML Files: This is the standard format required for most reports.

2. Digital Signatures: All documents must be digitally signed to ensure their authenticity and validity.

3. Online Platform: Submission is made through the platform enabled by the District Treasury Deparment, where the corresponding files must be uploaded.

Consequences of Non-Compliance

Failure to submit exogenous information by the established deadlines can result in significant financial penalties and other legal inconveniences. Fines for omission or late submission can severely impact the finances of a company or individual. Additionally, non-compliance can lead to tax investigations and audits.

At BéndiksenLaw, we understand the importance of complying with all tax obligations to avoid penalties and ensure peace of mind for our clients. Our team of tax law experts is ready to advise and assit your company throughout the exogenous information filing process.

Don’t let tax obligations catch you by surprise. Contact BéndiksenLaw for personalized advice and ensure compliance with exogenous information filing in Bogotá.

The regulatory landscape for food in Colombia has undergone significant transformation in recent years, especially with the implementation of Resolution 810 of 2021, subsequently modified by Resolutions 2492 of 2022 and 254 of 2023. These regulations establish specific requirements for nutrient declaration, the nutritional information table, and front-of-package warning labels for foods marketed in the country.

Nutrient Declaration

The nutrient declaration is an essential component of these regulations. This section requires food manufacturers to include detailed information about the nutrient content in their products. This includes macronutrients such as carbohydrates, proteins, and fats, as well as micronutrients like vitamins and minerals. The purpose of this declaration is to provide consumers with a clear and accurate view of the nutritional value of the foods they consume, facilitating informed and healthy decisions.

Nutritional Information Table

The nutritional information table complements the nutrient declaration by providing a structured and easy-to-understand format for presenting these data. This table must include information on energy value, total and saturated fat content, cholesterol, sodium, total carbohydrates, dietary fiber, total and added sugars, proteins, and certain essential micronutrients.

The modifications introduced by Resolution 2492 of 2022 and Resolution 254 of 2023 have refined the requirements for the nutritional information table, ensuring it is more comprehensible and useful for consumers. For instance, the size of the font and the format of the table have been specified, ensuring it is easily readable and accessible to all.

Front-of-Package Warning Labels

One of the most visible and debated aspects of these regulations is the front-of-package warning labels, represented by black octagonal seals. These labels are mandatory for products that contain high levels of certain components that can be harmful to health if consumed in excess, such as added sugars, sodium, and saturated fats.

The purpose of these labels is to quickly and effectively alert consumers about the potential risks associated with consuming these products. According to the regulations, foods that exceed the established limits for these nutrients must carry one or more warning labels on the front of the package.

Starting on June 15, 2024, all foods marketed in Colombia must comply with the provisions set out in Resolutions 810 of 2021, 2492 of 2022, and 254 of 2023. Products that do not meet these regulations must be removed from the market, except those with specific authorization to deplete existing labels.

The implementation of these resolutions presents significant challenges for food manufacturers and marketers, who must adapt quickly to these new requirements. It is essential that companies conduct a careful analysis of these regulations to ensure their labels comply with all applicable provisions.

In this context, having the right advice is crucial. At BéndiksenLaw, we have counseled multinational companies on food and additive regulations, helping them navigate the complex regulatory landscape in Colombia. If you need assistance to ensure compliance with these new regulations, do not hesitate to contact us.

The 2022 tax reform introduced, with effect from November 1, 2023, a tax classified as healthy, called the tax on industrially ultra-processed edible products and/or with a high content of added sugars, sodium or saturated fats (hereinafter the “ICUI” for its acronym in Spanish).

REASONING IN THE BILL SUBMITTED TO CONGRESS

The ICUI does not pursue collection purposes, strictly speaking.

According to the reasoning in the bill sent to Congress:

“On the other hand, ultra-processed foods, also known as ‘junk food’, have been the cause of chronic non-communicable diseases, such as hypertension, obesity, diabetes and some types of cancer, generating an expense to the health system of approximately 25 trillion pesos per year (2.1% of GDP) (Portfolio, 2022).

“One way to reduce the negative externalities associated with the consumption of sugar-sweetened beverages and ultra-processed foods is to implement a consumption tax on these products. These types of taxes correspond to a Pigouvian measure, and are generally used to reduce the consumption of some goods that result in negative externalities on the health of the population, in order to reduce the expenses of the health system associated with the incidence of diseases derived from the consumption of sugary drinks and ultra-processed foods and improve the well-being of the population.”

As can be seen, the ICUI is planned to correct the negative externality derived from the consumption of junk food on the health of the population through two mechanisms: the disincentive to their consumption and the generation of public resources that contribute to financing the requirements of the health system derived from related diseases.

THE TAX STATUTE PROVISIONS

The ICUI is regulated in articles 513-6 to 513-13 of the Tax Code.

In accordance with these provisions, the main features of the ICUI are as follows:

The Tax Administration

The tax administration of this levy is the Directorate of National Taxes and Customs (“DIAN” for its acronym in Spanish).

Taxable Persons

The producer and/or importer of these products, as the case may be, are responsible for the ICUI.

Taxable Events

Except for exports and certain donations that are excepted, the ICUI taxes:

The production, sale, removal of inventories or acts involving the transfer of ownership free of charge or for consideration of these products.

The importation of the aforementioned edible products.

However, it should be noted that this tax is not levied on all such edible products, but only those that have added sugars, salt/sodium and/or fats as ingredients and their content in the nutritional table exceeds the following values:

To calculate the percentages established in the table, the procedure in Paragraph 1 of Article 513-6 of the Tax Code should be followed. Paragraph 1, in addition to establishing the procedure to determinie the values, makes an extremely important clarification, namely, that, in the case of imported goods, the values of sodium, sugar and/or saturated fat content in the nutritional table must be reported in the import declaration. In other words, it will be based on the values contained in line 90 of the import declaration that, at the time of nationalization, determination is to e made as to whether or not the payment of the ICUI is appropriate.

But, as an additional limitation, only goods of the following tariff headings and subheadings are subject to ICUI, to the extent that they contain sodium, sugars or saturated fats in accordance with the definitions referred to below:

Taxable Base

The taxable base of this tax is the sales price.

In the case of donations or removal of inventory, the taxable base is the commercial value.

In the case of imported godos the taxable base on which the ICUI is to be calculated will be the same as that taken into account to settle customs taxes, increased by the value of this tax.

In the case of finished products produced in free zones, the taxable base will be the value of all production costs and expenses in accordance with the integration certificate plus the value of customs taxes. When the importer is the buyer or customer in the national customs territory, the taxable base will be the value of the invoice plus customs. taxes

Tax Rate

The tax rate is determined as follows:

Triggering Events

The ICUI is triggered as follows:

Definitions:

Article 513-6 of the Tax Code contains the following definitions:

Ultra-processed products are industrial formulations made from substances derived from food or synthesized from other organic sources. Some substances used to make ultra-processed products, such as fats, oils, starches and sugar, are derived directly from food. Others are obtained through the further processing of certain food components, such as the hydrogenation of oils (which generates toxic trans fats), the hydrolysis of proteins, and the “purification” of starches. The vast majority of ingredients in most ultra-processed products are additives (binders, cohesives, colours, sweeteners, emulsifiers, thickeners, foamers, stabilisers, sensory ”enhancers” such as flavourings and flavourings, preservatives, flavourings and solvents).

Ultra-processed products are industrial formulations mainly based on substances extracted or derived from food, as well as additives and cosmetics that give color, flavor or texture to try to imitate food. They are high in added sugars, total fat, saturated fat, and sodium, and low in protein, dietary fiber, minerals, and vitamins, compared to unprocessed or minimally processed products, dishes, and meals.

Ultra-processed products are understood as having salt/sodium added to them; those to which any salt or additive containing sodium or any ingredient containing added sodium salts has been used as an ingredient or additive during the manufacturing process.

An ultra-processed product shall be understood as having fats added to it; those to which vegetable or animal fats, partially hydrogenated vegetable oils (vegetable shortening, vegetable cream or margarine) and ingredients containing added greases have been used as ingredients during the manufacturing process.

Added sugars are monosaccharides and/or disaccharides that are added during food processing or packaged as such, and include those contained in syrups, fruit or vegetable juice concentrates.

Processed and/or ultra-processed food product that have added sugars will be understood as those to which sugars have been added during the manufacturing process according to the definition of the previous paragraph.

Additional Considerations

Cancelled, rescinded or terminated transactions of the related to the products subject to the ICUI will result in a lower value of the tax payable, without giving rise to a refund.

The ICUI constitutes for the buyer a deductible cost in income tax as a higher value of the product, under the terms of article 115 of the Tax Code.

The ICUI does not generate deductible taxes on sales tax – VAT.

The ICUI must be itemized in the sales invoice, in addition to the sales tax -/VA itemized on the invoice.

The taxable period for ICUI will be bimonthly. The bimonthly periods are: January-February, March-April, May-June, July-August, September-October, November-December.

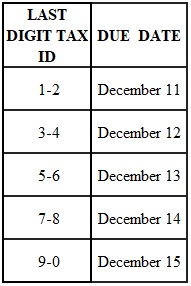

The deadlines to file the returns and pay the ICUI, other than the ICUI corresponding to imports, will be as follows:

The deadline to pay the taxes corresponding to the November-December 2023 two-month period will be extended from January 10th to the 23rd, 2024, according to the last digit of the TIN.

In the case of imports, the tax will be assessed and paid together with the settlement and payment of customs taxes, using forms 500, 505 and 690.

The ICUI return will not be filed in periods in which no transactions subject to these taxes have been carried out.

The penalty for non-payment of the ICUI is 20% of the value of the tax that has to be paid or 10% of the gross income that appears in the last tax return.

DIAN RULINGS

With respect to this tax, the DIAN has issued various rulings, among which we may highlight the following points:

The manufacturer of the inputs or ingredients used to manufacture the products subject to the ICUI is not liable for the ICUI, as would be the case – by way of example – of the producer of sugar, fats, oils and starches. The foregoing, unless such inputs or ingredients, individually considered, correspond to ultra-processed sugary beverages (including concentrates, powders and syrups) or to industrially ultra-processed edible products and/or with a high content of added sugars, sodium or saturated fats in the terms defined by the Law.

The inputs or ingredients used to make industrially ultra-processed edible products and/or with a high content of added sugars, sodium or saturated fats are not taxed with the ICUI, unless such inputs or ingredients, individually considered, correspond to industrially ultra-processed edible products and/or with a high content of added sugars, sodium or saturated fats in the terms defined by law.

The taxable base of the ICUI on imports consists of the sum of the customs value, customs duties, other duties, taxes or surcharges levied on importation or on the occasion of importation and VAT.

It is essential that all the legal requirements are met for a product to be considered taxed with the ICUI, one of which is that the product is edible. In this regard, the Dictionary of the Spanish Language contains the following:

(i) “Edible” is that which can be eaten.

(ii) “Eating” means “Chewing and swallowing solid food”.

Therefore, dietary supplements and reconstitution powders that are designed to be ingested in liquid form are not considered edible for the purposes discussed here. Therefore, they do not generate ICUI.

In relation to sodium, the legislator did not distinguish between added sodium and that which is naturally part of the edible product.

In relation to sugars and fats, only free sugars and saturated fats are taken into account. Therefore, for tax purposes, sugars and fats other than the above that are part of the edible product should not be taken into account.

To illustrate the above: If an edible product in its natural state has 299 milligrams of sodium per 100 grams and 2 milligrams of sodium per 100 grams are added to it, it would exceed the value from which the product is considered taxed with the ICUI (≥ 300 milligrams per 100 grams).

The definitions contained in Article 513-6 of the Tax Code on processed and/or ultra-processed products that “have added salt/sodium”, “have added fats” and “have added sugars” are not cumulative, although they may concur with each other; therefore, it will be sufficient for one of them to be present for purposes of the ICUI.

The information related to the ICUI must be included in the XML of the electronic invoice, under Code 35

As of December 1, 2023, discrimination (…) must be carried out under the terms set forth in the technical annex to electronic sales invoice version 1.9

Finally, although it is not a ruling per se, in a document related to the inflationary effects of the ICUI, the DIAN stated that the products taxed with the ICUI will be those that, as ingredients, have been added sugars, salt/sodium or fats sufficient to carry the front warning label established by the Ministry of Health.

CONCLUSION

The rules of the Tax Statute and the rulings issued by the DIAN, discussed above, leave open a good number of issues.

BéndiksenLaw has the experience and team to assist you with any concerns you may have regarding this lien. Contact us.

BéndiksenLaw is proud to announce its recent membership in the U.S. Chamber of Commerce, a world-leading organization in advocating for business interests. With its motto of advocating, connecting, informing, and fighting for business growth and success, this affiliation marks a significant milestone for our firm.

The U.S. Chamber of Commerce, known as the largest business organization in the world, encompasses everything from small businesses and local chambers of commerce to leading industrial associations and global corporations. For BéndiksenLaw, joining this prestigious network means accessing an unparalleled platform of business connections, learning opportunities, and a stronger voice in advocating for trade and investment-friendly policies.

At BéndiksenLaw, we have always been committed to growth and innovation, and this new partnership with the U.S. Chamber of Commerce allows us to further expand our reach and capabilities. This step is an affirmation of our dedication to providing quality international legal services and our desire to drive economic growth and prosperity in both Colombia and the global stage.

We invite our clients and partners to discover how this new strategic alliance can benefit their businesses. Together, with the support and resources of the U.S. Chamber of Commerce, we are ready to face tomorrow’s challenges and blaze new trails in the world of international trade and investment.

Contact us to learn more about how we can help you make the most of this exciting new chapter for BéndiksenLaw.

In the complex Colombian business and tax world, Transfer Pricing plays a crucial role. Multinational companies engaging in transactions with each other must comply with this regime to ensure fair taxation. Here, at BéndiksenLaw, we break down the obligations and deadlines you need to keep in mind for the upcoming December 2023.

Transfer Pricing focuses on assigning values to transactions between related companies in different jurisdictions. In Colombia, these obligations apply to companies conducting operations with affiliated entities abroad, in free trade zones, or in low-tax jurisdictions.

Formal obligations: What should you do?

Informative Return: Companies with assets exceeding 100,000 tax units (UVT) or annual income surpassing 61,000 UVT must file it.

Local Report: If transactions with economic affiliates exceed 45,000 UVT or involve entities in low or no-tax jurisdictions, filing this report is required.

Master Report: For taxpayers consolidating financial statements in multinational groups.

Country-by-Country Report: Applicable to the parent company or corporate office of the multinational group, filing is necessary for those meeting certain conditions.

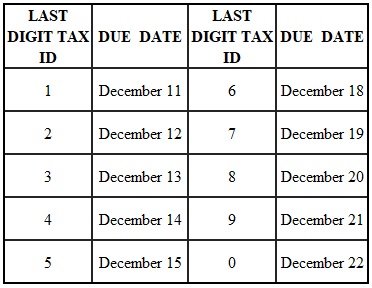

December deadlines: Act in advance

From December 11 to 22, based on the last digit of the Tax ID number (NIT), companies must submit master and country-by-country reports to the tax administration (DIAN), for fiscal year 2022. Ignoring these dates can result in penalties and legal issues.

Claudia González Béndiksen, partner at BéndiksenLaw, emphasizes, “Complying with these obligations is essential to ensure fair taxation and avoid penalties. Companies must stay informed about the requirements to contribute to a transparent and fair business environment in Colombia.”

Master Report – Fiscal Year 2022

Country-by-Country Report – Fiscal Year 2022

Act now! Ensure you meet these deadlines to maintain transparency and fairness in your business transactions.

After discussing the topic of international arbitration in Colombia, our managing partner and BéndiksenLaw have received notable mentions in various media outlets, including Diario La Economía, Valor Y Dinero, Economía en Serio, Revista Alternativa, Marcas y Estrategias and many others.

Don’t miss the opportunity to learn more about this relevant interview.

In the business sphere, the law establishes the bases that guide the operation and management of companies. Without a firm understanding of the legal framework, they could face challenges that hinder their trajectory to success. For this reason, events such as the Student Business Trial Contest, organized by the Bogotá Chamber of Commerce, are crucial as they provide a platform where the next generation of legal and business professionals can interact, learn and grow.

This year, we are honored to announce that BéndiksenLaw’s Managing Partner, Sebastián Béndiksen, will participate as a judge in the competition that will take place on Friday, October 27. With a distinguished track record in the corporate legal field, Sebastián Béndiksen represents BéndiksenLaw’s dedication, experience and commitment to excellence and continuing education. The participation of our managing partner as a judge underlines the importance that BéndiksenLaw places on the connection between academia and professional practice. This competition is an opportunity for students to experience the practical application of legal concepts in a business setting, while receiving valuable feedback from experts in the industry.

At BéndiksenLaw, we are proud to be part of initiatives that nurture knowledge and collaboration between the legal and business sectors. Our firm is committed to providing exceptional legal solutions that meet the unique needs of each client in today’s dynamic business environment. We invite you to learn more about how BéndiksenLaw can assist you with your legal needs and how our experience and collaborative approach can provide the legal support your firm needs to thrive.

The business world is a dynamic and constantly evolving field, where interaction between different actors is crucial for development and expansion. Along these lines, the 2023 International Business Meeting, organized by the Colombian-American Chamber of Commerce, stands as a privileged platform for meeting and collaboration between national and international companies. BéndiksenLaw, as an active member of this Chamber, participated in the event, represented by our managing partner, Sebastián Béndiksen.

AmCham Colombia, responsible for the event, has as its mission to promote trade relations between Colombia and the United States, and the 2023 International Business Meeting was a palpable manifestation of this objective. With the participation of more than 100 goods and services companies from more than 10 countries, the event offered a place for the formation of alliances, the discovery of new market trends, the strengthening of brand positioning, and the increase of knowledge in good business practices at national and international levels.

Sebastián Béndiksen’s participation not only represented BéndiksenLaw, but also marked the third time that our firm has been part of these significant encounters. These events reiterate our position and active commitment in international trade, highlighting the continuity and consistency in our contribution to strengthening trade relations between Colombia and the United States.

We invite you to explore more about how BéndiksenLaw can assist in navigating the complex legal landscape that accompanies international business relationships. Our firm is committed to providing exceptional legal counsel that enables businesses to operate with confidence on the global stage.

Contact us and find out how we can be the legal partner your company needs to thrive in the international arena.