The reporting of exogenous information is a key process that, under various circumstances, must be fulfilled by companies and individuals, whether or not they are taxpayers of the Industry and Commerce Tax in Bogotá, withholding agents of this tax, subjects of such withholdings, and others. This tax obligation is essential to ensure transparency and the correct reporting of economic activities to the tax authorities.

What is Exogenous Information?

Exogenous information is the set of data that obligated parties must report to the District Treasury Department of Bogotá about their economic, financial, and commercial operations. These reports allow authorities to conduct effective tax control and detect potential tax evasion.

Filing Deadlines

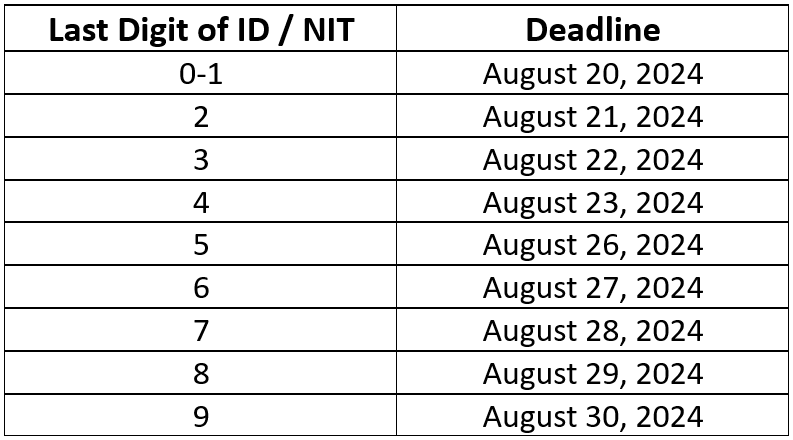

For 2024, the deadlines for filing exogenous information in Bogotá are clearly established, and it is crucial to comply with them to avoid penalties. Responsible parties must submit the corresponding information between August 20 and 30, 2024, according to the last digit of their ID or Tax ID Number (NIT):

It is important to be mindful of these deadlines and prepare all necessary documentation in advance.

Filing Method

Exogenous information must be submitted in magnetic media, following the formats and technical specifications established by the District Treasury Deparment. Ensuring that the reports meet all technical requirements is crucial to avoid rejections and possible penalties. The filing method includes:

1. XML Files: This is the standard format required for most reports.

2. Digital Signatures: All documents must be digitally signed to ensure their authenticity and validity.

3. Online Platform: Submission is made through the platform enabled by the District Treasury Deparment, where the corresponding files must be uploaded.

Consequences of Non-Compliance

Failure to submit exogenous information by the established deadlines can result in significant financial penalties and other legal inconveniences. Fines for omission or late submission can severely impact the finances of a company or individual. Additionally, non-compliance can lead to tax investigations and audits.

At BéndiksenLaw, we understand the importance of complying with all tax obligations to avoid penalties and ensure peace of mind for our clients. Our team of tax law experts is ready to advise and assit your company throughout the exogenous information filing process.

Don’t let tax obligations catch you by surprise. Contact BéndiksenLaw for personalized advice and ensure compliance with exogenous information filing in Bogotá.

In a globalized world, companies with operations in multiple countries face unique challenges in terms of tax compliance. One of the most critical areas is transfer pricing, which refers to the prices at which companies within the same group conduct any type of transaction among themselves, such as the purchase and sale of products or assets, provision of services, granting of loans, among others. Adequate international tax planning is key to optimizing these transfer prices and ensuring both efficiency and regulatory compliance.

What is Transfer Pricing?

Transfer pricing refers to the prices at which transactions are conducted between companies that belong to the same corporate group but operate in different jurisdictions. This mechanism is essential for the correct distribution of income and expenses among the various entities of a corporate group, ensuring that they are reflected fairly and in accordance with the tax laws of each country.

The Importance of International Tax Planning

Effective international tax planning allows companies not only to comply with local and international regulations but also to optimize their tax burden. In Colombia, the regulatory framework for transfer pricing aims for transparency and fair tax contributions, aligned with OECD practices. However, without an adequate strategy, companies may face significant tax adjustments and penalties.

A well-planned transfer pricing strategy can offer several benefits, such as the reduction of legal and financial risks, tax optimization, and improvement in business and financial planning. By staying up-to-date with tax regulations, companies can avoid costly penalties and litigation. Through an effective strategy, it is possible to achieve an efficient tax burden, thereby maximizing the profitability of the corporate group.

At BéndiksenLaw, we understand the complexity of the global tax environment and offer specialized services in transfer pricing. We analyze your company’s current transfer pricing policies and suggest adjustments to align them with recommended international practices. Additionally, we assist in preparing all necessary documentation to comply with Colombian regulations and reduce the risk of tax adjustments.

If your company operates internationally and seeks to optimize its transfer pricing strategy, contact BéndiksenLaw. Our experts are ready to help you navigate the complexities of the international tax environment and ensure that your company complies with all regulations while maximizing its tax efficiency.

The regulatory landscape for food in Colombia has undergone significant transformation in recent years, especially with the implementation of Resolution 810 of 2021, subsequently modified by Resolutions 2492 of 2022 and 254 of 2023. These regulations establish specific requirements for nutrient declaration, the nutritional information table, and front-of-package warning labels for foods marketed in the country.

Nutrient Declaration

The nutrient declaration is an essential component of these regulations. This section requires food manufacturers to include detailed information about the nutrient content in their products. This includes macronutrients such as carbohydrates, proteins, and fats, as well as micronutrients like vitamins and minerals. The purpose of this declaration is to provide consumers with a clear and accurate view of the nutritional value of the foods they consume, facilitating informed and healthy decisions.

Nutritional Information Table

The nutritional information table complements the nutrient declaration by providing a structured and easy-to-understand format for presenting these data. This table must include information on energy value, total and saturated fat content, cholesterol, sodium, total carbohydrates, dietary fiber, total and added sugars, proteins, and certain essential micronutrients.

The modifications introduced by Resolution 2492 of 2022 and Resolution 254 of 2023 have refined the requirements for the nutritional information table, ensuring it is more comprehensible and useful for consumers. For instance, the size of the font and the format of the table have been specified, ensuring it is easily readable and accessible to all.

Front-of-Package Warning Labels

One of the most visible and debated aspects of these regulations is the front-of-package warning labels, represented by black octagonal seals. These labels are mandatory for products that contain high levels of certain components that can be harmful to health if consumed in excess, such as added sugars, sodium, and saturated fats.

The purpose of these labels is to quickly and effectively alert consumers about the potential risks associated with consuming these products. According to the regulations, foods that exceed the established limits for these nutrients must carry one or more warning labels on the front of the package.

Starting on June 15, 2024, all foods marketed in Colombia must comply with the provisions set out in Resolutions 810 of 2021, 2492 of 2022, and 254 of 2023. Products that do not meet these regulations must be removed from the market, except those with specific authorization to deplete existing labels.

The implementation of these resolutions presents significant challenges for food manufacturers and marketers, who must adapt quickly to these new requirements. It is essential that companies conduct a careful analysis of these regulations to ensure their labels comply with all applicable provisions.

In this context, having the right advice is crucial. At BéndiksenLaw, we have counseled multinational companies on food and additive regulations, helping them navigate the complex regulatory landscape in Colombia. If you need assistance to ensure compliance with these new regulations, do not hesitate to contact us.

The 2022 tax reform introduced, with effect from November 1, 2023, a tax classified as healthy, called the tax on industrially ultra-processed edible products and/or with a high content of added sugars, sodium or saturated fats (hereinafter the “ICUI” for its acronym in Spanish).

REASONING IN THE BILL SUBMITTED TO CONGRESS

The ICUI does not pursue collection purposes, strictly speaking.

According to the reasoning in the bill sent to Congress:

“On the other hand, ultra-processed foods, also known as ‘junk food’, have been the cause of chronic non-communicable diseases, such as hypertension, obesity, diabetes and some types of cancer, generating an expense to the health system of approximately 25 trillion pesos per year (2.1% of GDP) (Portfolio, 2022).

“One way to reduce the negative externalities associated with the consumption of sugar-sweetened beverages and ultra-processed foods is to implement a consumption tax on these products. These types of taxes correspond to a Pigouvian measure, and are generally used to reduce the consumption of some goods that result in negative externalities on the health of the population, in order to reduce the expenses of the health system associated with the incidence of diseases derived from the consumption of sugary drinks and ultra-processed foods and improve the well-being of the population.”

As can be seen, the ICUI is planned to correct the negative externality derived from the consumption of junk food on the health of the population through two mechanisms: the disincentive to their consumption and the generation of public resources that contribute to financing the requirements of the health system derived from related diseases.

THE TAX STATUTE PROVISIONS

The ICUI is regulated in articles 513-6 to 513-13 of the Tax Code.

In accordance with these provisions, the main features of the ICUI are as follows:

The Tax Administration

The tax administration of this levy is the Directorate of National Taxes and Customs (“DIAN” for its acronym in Spanish).

Taxable Persons

The producer and/or importer of these products, as the case may be, are responsible for the ICUI.

Taxable Events

Except for exports and certain donations that are excepted, the ICUI taxes:

The production, sale, removal of inventories or acts involving the transfer of ownership free of charge or for consideration of these products.

The importation of the aforementioned edible products.

However, it should be noted that this tax is not levied on all such edible products, but only those that have added sugars, salt/sodium and/or fats as ingredients and their content in the nutritional table exceeds the following values:

To calculate the percentages established in the table, the procedure in Paragraph 1 of Article 513-6 of the Tax Code should be followed. Paragraph 1, in addition to establishing the procedure to determinie the values, makes an extremely important clarification, namely, that, in the case of imported goods, the values of sodium, sugar and/or saturated fat content in the nutritional table must be reported in the import declaration. In other words, it will be based on the values contained in line 90 of the import declaration that, at the time of nationalization, determination is to e made as to whether or not the payment of the ICUI is appropriate.

But, as an additional limitation, only goods of the following tariff headings and subheadings are subject to ICUI, to the extent that they contain sodium, sugars or saturated fats in accordance with the definitions referred to below:

Taxable Base

The taxable base of this tax is the sales price.

In the case of donations or removal of inventory, the taxable base is the commercial value.

In the case of imported godos the taxable base on which the ICUI is to be calculated will be the same as that taken into account to settle customs taxes, increased by the value of this tax.

In the case of finished products produced in free zones, the taxable base will be the value of all production costs and expenses in accordance with the integration certificate plus the value of customs taxes. When the importer is the buyer or customer in the national customs territory, the taxable base will be the value of the invoice plus customs. taxes

Tax Rate

The tax rate is determined as follows:

Triggering Events

The ICUI is triggered as follows:

Definitions:

Article 513-6 of the Tax Code contains the following definitions:

Ultra-processed products are industrial formulations made from substances derived from food or synthesized from other organic sources. Some substances used to make ultra-processed products, such as fats, oils, starches and sugar, are derived directly from food. Others are obtained through the further processing of certain food components, such as the hydrogenation of oils (which generates toxic trans fats), the hydrolysis of proteins, and the “purification” of starches. The vast majority of ingredients in most ultra-processed products are additives (binders, cohesives, colours, sweeteners, emulsifiers, thickeners, foamers, stabilisers, sensory ”enhancers” such as flavourings and flavourings, preservatives, flavourings and solvents).

Ultra-processed products are industrial formulations mainly based on substances extracted or derived from food, as well as additives and cosmetics that give color, flavor or texture to try to imitate food. They are high in added sugars, total fat, saturated fat, and sodium, and low in protein, dietary fiber, minerals, and vitamins, compared to unprocessed or minimally processed products, dishes, and meals.

Ultra-processed products are understood as having salt/sodium added to them; those to which any salt or additive containing sodium or any ingredient containing added sodium salts has been used as an ingredient or additive during the manufacturing process.

An ultra-processed product shall be understood as having fats added to it; those to which vegetable or animal fats, partially hydrogenated vegetable oils (vegetable shortening, vegetable cream or margarine) and ingredients containing added greases have been used as ingredients during the manufacturing process.

Added sugars are monosaccharides and/or disaccharides that are added during food processing or packaged as such, and include those contained in syrups, fruit or vegetable juice concentrates.

Processed and/or ultra-processed food product that have added sugars will be understood as those to which sugars have been added during the manufacturing process according to the definition of the previous paragraph.

Additional Considerations

Cancelled, rescinded or terminated transactions of the related to the products subject to the ICUI will result in a lower value of the tax payable, without giving rise to a refund.

The ICUI constitutes for the buyer a deductible cost in income tax as a higher value of the product, under the terms of article 115 of the Tax Code.

The ICUI does not generate deductible taxes on sales tax – VAT.

The ICUI must be itemized in the sales invoice, in addition to the sales tax -/VA itemized on the invoice.

The taxable period for ICUI will be bimonthly. The bimonthly periods are: January-February, March-April, May-June, July-August, September-October, November-December.

The deadlines to file the returns and pay the ICUI, other than the ICUI corresponding to imports, will be as follows:

The deadline to pay the taxes corresponding to the November-December 2023 two-month period will be extended from January 10th to the 23rd, 2024, according to the last digit of the TIN.

In the case of imports, the tax will be assessed and paid together with the settlement and payment of customs taxes, using forms 500, 505 and 690.

The ICUI return will not be filed in periods in which no transactions subject to these taxes have been carried out.

The penalty for non-payment of the ICUI is 20% of the value of the tax that has to be paid or 10% of the gross income that appears in the last tax return.

DIAN RULINGS

With respect to this tax, the DIAN has issued various rulings, among which we may highlight the following points:

The manufacturer of the inputs or ingredients used to manufacture the products subject to the ICUI is not liable for the ICUI, as would be the case – by way of example – of the producer of sugar, fats, oils and starches. The foregoing, unless such inputs or ingredients, individually considered, correspond to ultra-processed sugary beverages (including concentrates, powders and syrups) or to industrially ultra-processed edible products and/or with a high content of added sugars, sodium or saturated fats in the terms defined by the Law.

The inputs or ingredients used to make industrially ultra-processed edible products and/or with a high content of added sugars, sodium or saturated fats are not taxed with the ICUI, unless such inputs or ingredients, individually considered, correspond to industrially ultra-processed edible products and/or with a high content of added sugars, sodium or saturated fats in the terms defined by law.

The taxable base of the ICUI on imports consists of the sum of the customs value, customs duties, other duties, taxes or surcharges levied on importation or on the occasion of importation and VAT.

It is essential that all the legal requirements are met for a product to be considered taxed with the ICUI, one of which is that the product is edible. In this regard, the Dictionary of the Spanish Language contains the following:

(i) “Edible” is that which can be eaten.

(ii) “Eating” means “Chewing and swallowing solid food”.

Therefore, dietary supplements and reconstitution powders that are designed to be ingested in liquid form are not considered edible for the purposes discussed here. Therefore, they do not generate ICUI.

In relation to sodium, the legislator did not distinguish between added sodium and that which is naturally part of the edible product.

In relation to sugars and fats, only free sugars and saturated fats are taken into account. Therefore, for tax purposes, sugars and fats other than the above that are part of the edible product should not be taken into account.

To illustrate the above: If an edible product in its natural state has 299 milligrams of sodium per 100 grams and 2 milligrams of sodium per 100 grams are added to it, it would exceed the value from which the product is considered taxed with the ICUI (≥ 300 milligrams per 100 grams).

The definitions contained in Article 513-6 of the Tax Code on processed and/or ultra-processed products that “have added salt/sodium”, “have added fats” and “have added sugars” are not cumulative, although they may concur with each other; therefore, it will be sufficient for one of them to be present for purposes of the ICUI.

The information related to the ICUI must be included in the XML of the electronic invoice, under Code 35

As of December 1, 2023, discrimination (…) must be carried out under the terms set forth in the technical annex to electronic sales invoice version 1.9

Finally, although it is not a ruling per se, in a document related to the inflationary effects of the ICUI, the DIAN stated that the products taxed with the ICUI will be those that, as ingredients, have been added sugars, salt/sodium or fats sufficient to carry the front warning label established by the Ministry of Health.

CONCLUSION

The rules of the Tax Statute and the rulings issued by the DIAN, discussed above, leave open a good number of issues.

BéndiksenLaw has the experience and team to assist you with any concerns you may have regarding this lien. Contact us.

This Wednesday we had the privilege of being represented at AndinaPack 2023 with a talk by Sebastián Béndiksen, managing partner of BéndiksenLaw, in the Legal Forum “How Can Legal Tools Contribute to Circularity?” Sebastián, with his experience in the food and additives sector, tackled a crucial topic: compliance with regulations and labeling requirements in the food industry.

His presentation delved into how comprehensive knowledge of food and labeling regulations is essential for successful operation in the Colombian market. Sebastián emphasized that adhering to current regulations is not only a legal obligation but also a guarantee of quality and trust for consumers and a safeguard against potential sanctions. He highlighted the responsibility of companies to stay updated and comply with legislation to ensure their continuity and growth in the market.

Sebastián’s intervention served not only to illustrate the importance of regulatory compliance but also to underscore how BéndiksenLaw, with its expert and dedicated team, can be a strategic ally in this process. We believe that keeping up with regulations is not just a matter of compliance but also an opportunity to improve business practices and strengthen market confidence. Through the legal advice and guidance we offer, we help companies navigate the complex legal framework governing the food industry.

Our commitment to excellence and integrity in legal advice motivates us to continue actively participating in events like Andina Pack, where we can share our knowledge and learn from other industry leaders.

We invite those interested in these topics to visit our website for more information and discover how we can support them in complying with food and labeling regulations, a key step in ensuring the success and sustainability of their operations in the Colombian market.

BéndiksenLaw is proud to announce its recent membership in the U.S. Chamber of Commerce, a world-leading organization in advocating for business interests. With its motto of advocating, connecting, informing, and fighting for business growth and success, this affiliation marks a significant milestone for our firm.

The U.S. Chamber of Commerce, known as the largest business organization in the world, encompasses everything from small businesses and local chambers of commerce to leading industrial associations and global corporations. For BéndiksenLaw, joining this prestigious network means accessing an unparalleled platform of business connections, learning opportunities, and a stronger voice in advocating for trade and investment-friendly policies.

At BéndiksenLaw, we have always been committed to growth and innovation, and this new partnership with the U.S. Chamber of Commerce allows us to further expand our reach and capabilities. This step is an affirmation of our dedication to providing quality international legal services and our desire to drive economic growth and prosperity in both Colombia and the global stage.

We invite our clients and partners to discover how this new strategic alliance can benefit their businesses. Together, with the support and resources of the U.S. Chamber of Commerce, we are ready to face tomorrow’s challenges and blaze new trails in the world of international trade and investment.

Contact us to learn more about how we can help you make the most of this exciting new chapter for BéndiksenLaw.

In the complex Colombian business and tax world, Transfer Pricing plays a crucial role. Multinational companies engaging in transactions with each other must comply with this regime to ensure fair taxation. Here, at BéndiksenLaw, we break down the obligations and deadlines you need to keep in mind for the upcoming December 2023.

Transfer Pricing focuses on assigning values to transactions between related companies in different jurisdictions. In Colombia, these obligations apply to companies conducting operations with affiliated entities abroad, in free trade zones, or in low-tax jurisdictions.

Formal obligations: What should you do?

Informative Return: Companies with assets exceeding 100,000 tax units (UVT) or annual income surpassing 61,000 UVT must file it.

Local Report: If transactions with economic affiliates exceed 45,000 UVT or involve entities in low or no-tax jurisdictions, filing this report is required.

Master Report: For taxpayers consolidating financial statements in multinational groups.

Country-by-Country Report: Applicable to the parent company or corporate office of the multinational group, filing is necessary for those meeting certain conditions.

December deadlines: Act in advance

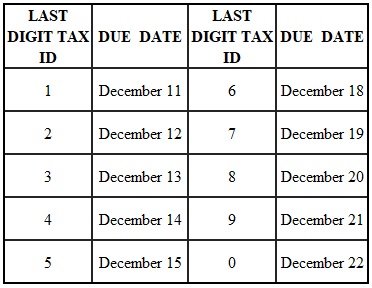

From December 11 to 22, based on the last digit of the Tax ID number (NIT), companies must submit master and country-by-country reports to the tax administration (DIAN), for fiscal year 2022. Ignoring these dates can result in penalties and legal issues.

Claudia González Béndiksen, partner at BéndiksenLaw, emphasizes, “Complying with these obligations is essential to ensure fair taxation and avoid penalties. Companies must stay informed about the requirements to contribute to a transparent and fair business environment in Colombia.”

Master Report – Fiscal Year 2022

Country-by-Country Report – Fiscal Year 2022

Act now! Ensure you meet these deadlines to maintain transparency and fairness in your business transactions.

We will find out about the legal competition of cryptoassets in Colombian companies from Sebastián Béndiksen, managing partner of BéndiksenLaw and specialist in corporate law. Sebastián shares with us his experience and key advice on the subject, guides us through the legal implications and responsibility of administrators in this constantly evolving area.

In this exclusive webinar we explore the current legal landscape of cryptocurrencies in Colombia, the necessary security measures, and the tax implications that must be taken into account.

Do not miss the opportunity to obtain valuable information and clear your doubts about the compliance of cryptoassets in Colombian companies.

Remember that at BéndiksenLaw you will find the support and advice you need to successfully navigate the legal implications and responsibilities. Do not hesitate to contact us!

Watch the webinar (in Spanish)

To download the presentation (in Spanish) click here

Are you interested in learning more about cryptoasset legal compliance and how it applies to businesses in Colombia? If so, we have great news for you! We are organizing an exciting webinar (in Spanish) that will take place on June 6 at 10:30 am, where we will delve into the essential knowledge that every Colombian company must consider in the world of cryptoassets. If you want to keep your business up to date and make sure you comply with all regulations, this webinar is for you. Keep reading to learn more!

Details of the event:

Date: June 6, 2023

Time: 10:30 am (Colombia time)

In this webinar our managing partner, Sebastián Béndiksen, will give us valuable and practical information on how companies in Colombia can address the challenges and opportunities related to cryptoassets safely and in compliance with regulations.

Who should attend?

This webinar is designed for entrepreneurs, directors, managers, legal professionals and anyone interested in understanding the legal and regulatory aspects of cryptoassets in the Colombian context. It does not matter if you already have experience in the subject or if you are new to the world of cryptoactives, this event will give you valuable and updated information.

Do not miss this opportunity to acquire essential knowledge about legal compliance of cryptoassets and how to apply them to your company in Colombia. The webinar on June 6 at 10:30 am will be an invaluable opportunity to stay updated and ensure you comply with regulations in the world of cryptoassets. Register now and reserve your spot. We are waiting for you!

On December 13, 2022, Colombia enacted Law 2277, embodying the most recent tax reform which came into effect on January 1, 2023 with some exceptions. In this article, our new Head of Tax explains several topics of the reform of interest to our clients.

I. Alternative Minimum Tax.

Inspired by the OECD BEPS global anti-base erosion (GloBE) rules Pillar Two recommendations, the tax reform introduces a new 15% alternative minimum tax for corporate taxpayers, including taxpayers operating in free-trade zones (“zonas francas”). This minimum tax does not apply to non-resident foreign entities.

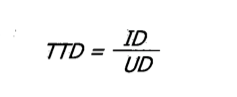

This minimum tax, called Net Tax Rate (Tasa de Tributación Depurada or “TTD” for its acronym in Spanish) is based on the taxpayer’s book profits (with certain adjustments), called Net Book Profit (Utilidad Depurada or “UD” for its acronym in Spanish).

The TTD paid by any given taxpayer, that is, its effective tax rate, is arrived at by dividing the taxpayer’s Net Income Tax (“ID”) by its Net Book Profit (“UD”). It is expressed in the law with the following formula:

Whenever the TTD computed under the above formula is lower than 15%, taxpayers must determine the amount of Additional Tax Due (“IA”) by multiplying the Net Book Profit (UD) by 15% and subtracting the Net Income Tax (ID):

For purposes of these calculations:

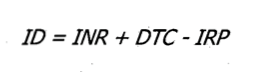

The Net Income Tax (ID) is the actual income tax paid (“INR”), increased by tax discounts or credits originating from tax treaties and by foreign tax credits (“DTC”), minus the income tax paid on passive income from foreign controlled entities (computed by applying the general 35% corporate tax rate to the taxable passive income) (“IRP”). The formula is:

The Net Book Profit (UD), in turn, is calculated under the following formula:

Where:

UC

is the book profit before taxes.

DAPARL

refers to permanent differences set forth in the law that increase taxable income.

INCRNGO

refers to income that is neither taxable income nor capital gains income and which affects book profits.

VIMPP

is the income determined under the equity method for the corresponding tax year.

VNGO

this is the net value of capital gains income affecting book profits.

RE

stands for exempt income originating from tax treaties, income received under the Colombian holding regime, exempt income on certain sales of social interest and priority interest housing and income received under certain pension funds

C

compensation of prior years’ net operating losses or excess of presumptive income, taken during the tax year and which did not affect the book profit for the tax year.

Special calculations apply for taxpayers consolidating financial results. In essence:

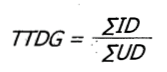

The Net Tax Rate for the Group (“TTDG”) is calculated by dividing the sum of the Net Income Tax of each Colombian resident taxpayer in the consolidation (“SID”) by the sum of the Net Profit of each such taxpayer (“SUD”):

Where the result is lower than 15%, the Additional Tax Due for the Group (“IAG”) is determined by the difference between the sum of the Net Book Profit for each Colombian resident taxpayer in the consolidation (SUD) multiplied by 15% less the sum of the Net Tax of each such taxpayer (SID):

In order to determine the Additional Tax (IA) for each Colombian resident taxpayer, the above result is multiplied by the factor resulting from dividing the Net Book Profit of each taxpayer higher than zero (“UDB”) by the sum of the Net Book Profit of all taxpayers in the group with Net Book Profits higher than zero (“SUDB”):

These alternative minimum tax rules do not apply to the following taxpayers:

Taxpayers who do not consolidate financial results and their Net Book Profit (“UD”) is zero or lower.

Taxpayers who consolidate financial results and the sum of all Net Book Profits (“SUD”) is zero or lower.

Entities incorporated as Special Economic and Social Zones (“Zonas Económicas y Sociales Especiales or “ZESE”).

Certain government-owned entities engaged in gambling or alcohol and liquor monopolistic activities.

II. Capital Gains

The rate for capital gains (“ganancias ocasionales”) generated by Colombian entities and by non-resident entities alike was increased from 10% to 15%.

III. Dividends

Dividends paid to nonresidents are subject to a 2-tier withholding tax calculation, as follows:

If the dividends originate from earnings that have not been previously taxed, then they will be taxed at the general 35% corporate tax rate.

The balance remaining after payment of the above tax is further subject to withholding tax. Here the tax rate was doubled by the tax reform, increasing from 10% to 20%.

IV. Free-Trade Zones

Entities carrying on operations in specified free-trade zones are entitled to a preferential 20% corporate tax rate, except for commercial users, to whom the general 35% tax rate applies.

Effective 2024, the tax reform sets the following distinctions:

Industrial users:

The ratable portion of taxable income corresponding to exportation of goods and services will be taxed at the preferential 20% rate. This will include health services provided in certain specific free-trade zones to patients residing outside Colombia.

This benefit is subject to the industrial free-zone users signing, with the Ministry of Commerce, Industry and Tourism, in 2023 or 2024, an internationalization and annual sales plan for each tax year, setting forth maximum goals for net income from operations of any kind within Colombia and income from activities other than their authorized activities.

Such a plan will be mandatory for entities securing free-trade zone authorization as from 2025.

Failure to sign the plan or to reach the maximum income goals will result in the benefit of the preferential tax rate being lost and thus being subject to the general 35% rate.

The ratable portion of all other taxable income will be subject to the general 35% corporate tax rate.

Commercial users:

Commercial free-zone users will continue to be taxed at the general 35% corporate tax rate.

Rules of Exception:

Industrial free-zone users with an increase of at least 60% in gross revenues in 2022 as compared to 2019 shall be entitled to apply a 20% tax rate through 2025.

Free-trade zone users who have signed with the Colombian government a so-called “legal stability agreement” (agreements basically freezing the tax provisions in place at the time they are signed and thus protecting against future changes in the tax law) will be subject to the tax rate called for in such agreement.

The preferential 20% corporate tax rate also applies to the following: offshore free-trade zones; industrial users of special permanent free-trade zones of port services, industrial users of port services in free zones (“zonas francas”), industrial users of special permanent free zones (“zonas francas”), whose main corporate purpose is refining of petroleum-derived fuels or refining of industrial biofuels; industrial users of certain qualifying logistics services and free zone (“zona franca”) operator users.

V. Research and Development Investments

The tax credit for investments in qualifying research and development is increased from 25% to 30%.

Cost and expenses qualifying for this tax credit cannot be capitalized or claimed as costs or deductions.

VI. Amnesties

The reform includes the following few amnesties:

Late-payment interest: the late payment interest on overdue taxes and customs dues paid on or before June 30, 2023, and on extensions granted by the tax administration on or before that same date is reduced by 50%. Applications for extensions must be filed not later than May 15, 2023.

VAT returns: VAT returns filed up to November 30, 2022, stating an incorrect tax period and thus null and void, may be filed up to April 30, 2023, with no late-filing penalty and no late-payment interest.

Taxpayers may, before May 31, 2023, file returns not filed up to December 31, 2022, paying the corresponding amounts due, with a reduction of 60% of the penalty that would apply after the reductions in Article 640 of the Tax Code and a 60% reduction in the interest rate. The same benefits apply where, in lieu of payment, these taxpayers request a payment agreement with the tax administration before May 31, 2023, and sign such agreement before June 30, 2023.

Taxpayers who have been served notices to file or amend tax returns or to pay taxes assessed, may pay the corresponding amounts on or before June 30, 2023, with a 20% reduction of the amount assessed. The reduction also applies to taxpayers who file for a payment agreement with the tax administration no later than May 15, 2023, and sign the corresponding agreement by June 30, 2023.

Should you have any questions, do not hesitate to contact us.